This article was contributed by Nimide Fala, Vice President of Client Experience at Zest, and Eytan Messika, Co-founder at Nilos as part of the Emerging Trends in Cross-Border Payments: A Growth Guide for Stakeholders report authored by Aroghene Favour Ndulu and Paschal Okeke.

For African businesses and consumers, cross-border payment solutions must nail four critical things: speed, affordability, accessibility, and reliability.

Small businesses need cash flow, so they want instant payments. Imagine an SME importing fabrics from China. If payments are delayed, goods get stuck, and cash flow suffers. Freelancers face the same issue when waiting on international payments.

Affordability can’t be ignored. High fees are a dealbreaker for most. Businesses, especially SMEs, operate on tight margins, so every dollar counts. They want affordable solutions with clear, transparent fees and no hidden surprises. A couple of fintech platforms are solving this by reducing transaction costs and offering predictable exchange rates, which makes life easier for businesses.

Accessibility is crucial. Not everyone has access to traditional banks; mobile money is often the go-to method in Africa. Solutions must work where businesses and consumers are, whether through mobile wallets, bank transfers, or local agents. M-Pesa is a great example. It’s made sending and receiving payments simple, even for micro-businesses in rural areas.

Trust is everything. Businesses and consumers need to know their money is safe, the process is secure, and payments will arrive on time, with no errors and no headaches. Fintech platforms can tackle this by investing in fraud prevention and real-time tracking so users can confidently send payments.

Solutions that get these basics enable growth, build trust, and make cross-border payments more seamless.

Improving speed and transparency

The solution is brutal simplicity. Most providers try to build complex systems, but the winners will be those who ruthlessly eliminate steps. Think early Amazon: one-click ordering worked because it removed friction. African payments need their “one-click” moment.

Bring blockchain into the picture. Blockchain improves speed and solves the “black hole” problem, where businesses wonder, “Where’s my money?” It creates a transparent, shared ledger that shows every transfer step.

Transparency also means communication. Real-time tracking, such as when monitoring a package, builds confidence. Send instant updates through email or an in-app so users know exactly where their payment is and when it will arrive.

Providers must work with local banks, mobile money platforms, and regional systems to move payments quickly. A global network means nothing if it can’t reach the last mile. Onafriq is a great example; it has connected directly with mobile wallets across Africa, ensuring payments arrive even in remote areas.

Pain points of SMES in cross-border payments

The biggest pain isn’t technical – it’s uncertainty. SMEs can’t predict when they’ll get paid or what it’ll cost. This unpredictability kills growth. It’s similar to what kills most startups: not running out of money, but running out of confidence about money.

Payments that take days to clear disrupt cash flow, supplier relationships, and customer experience. SMEs don’t have the luxury of waiting. They need funds to move quickly and stay competitive and agile.

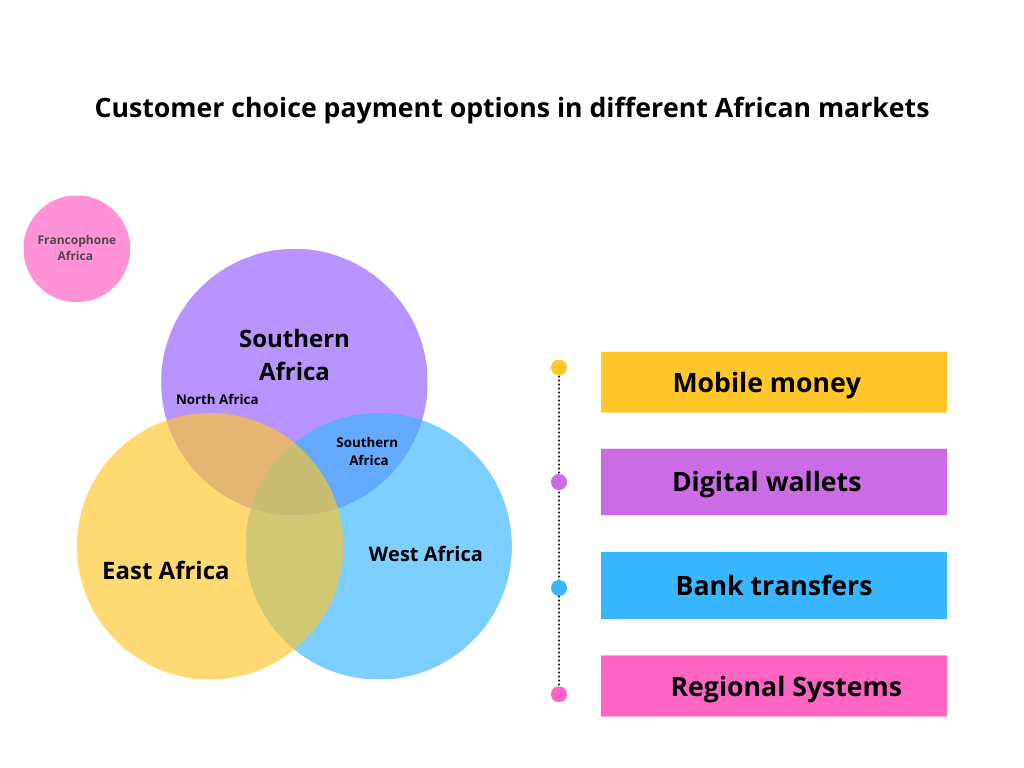

Understanding customer preferences

East Africa is the heartland of mobile money, led by pioneers like M-Pesa in Kenya and Tanzania. Mobile wallets are king for customers here because they’re fast, accessible, and don’t rely on traditional banks. Businesses and consumers often prioritise tools that integrate with these platforms seamlessly. For example, a Kenyan merchant receiving payments from Uganda will likely prefer M-Pesa-integrated solutions over bank transfers because they are quicker and more widely trusted. The mobile money infrastructure in East Africa is well established, and even small vendors in rural areas use it daily.

Volume of mobile money transactions in Africa in 2020 to 2022 (in billions), by region

Source: Statistica

Bank transfers dominate in West Africa, particularly Nigeria. The region relies more on banks than East Africa, and fintech solutions are often designed to integrate with existing banking systems. However, cash remains significant for many informal businesses.

Southern Africa, particularly South Africa, shows a mix of preferences. Businesses and consumers use digital wallets, bank transfers, and card payments. Platforms like Ozow and PayFast are popular for their focus on seamless digital payments, while traditional bank transfers remain relevant for larger transactions. Southern Africa has higher banking penetration and a tech-savvy population comfortable with digital wallets and online platforms.

Francophone Africa leans heavily on regional solutions like GIM-UEMOA {the interbank payment network) and local digital platforms like Orange Money. Customers here prioritise solutions that work across the West African Economic and Monetary Union {WAEMU), where the CFA Franc is shared. A business in Senegal paying a supplier in Cote d’Ivoire will often prefer platforms like Wave or Orange Money for cross-border transfers because they’re fast, affordable, and tailored for the region. Regional integration and shared currency make it easier to adopt localised solutions.

Meanwhile, North Africa, Egypt, and Morocco, particularly, rely heavily on bank transfers and the growing use of digital wallets. With strong trade ties to Europe, businesses prefer solutions that bridge local systems with international banking, while younger consumers are driving digital adoption forward.

Product and service localisation in cross-border payments

Product adoption happens faster when providers tailor their solutions to local realities like language, currency, and preferred payment methods. A platform might have great features, but if it’s not available in the local language, it becomes a barrier.

Constant currency conversions and reliance on US dollars add friction and costs. When businesses can pay and get paid in their local currency, it simplifies operations, cuts costs, and builds confidence to transact globally. It is also crucial to integrate local payment options to ease customer adaptability.

The best localisation is about fitting into existing behaviour patterns. M-PESA succeeded because it matched how Kenyans already handled money. That’s the key: build around existing behaviours, don’t try to change them.

You can read the full report here.

__________________

Nimide Fala is the Vice President of Client Experience at Zest, a fintech subsidiary of Stanbic IBTC Holdings. She is passionate about blending creativity and data for compelling storytelling and designing and executing effective product and data-led multi-media marketing strategies that drive business and revenue growth. Her over 13 years of experience is layered with proven records of success for established brands and startups such as Softcom Africa, Red Media Africa, Decagon Institute, etc.

Eytan Messika is the co-founder of Nilos, a fintech startup established in 2021 that provides a platform for businesses to unify their crypto wallets, bank accounts, and payment service providers, streamlining treasury operations across both crypto and fiat currencies. He is a seasoned entrepreneur and financial technology innovator with a background in both applied mathematics and business strategy.