Highlights

A jump in performance provided an early holiday gift for hoteliers

Nine of every 10 U.S. markets posted RevPAR gains

Group demand looks unstoppable

Second highest Global RevPAR gain of the year

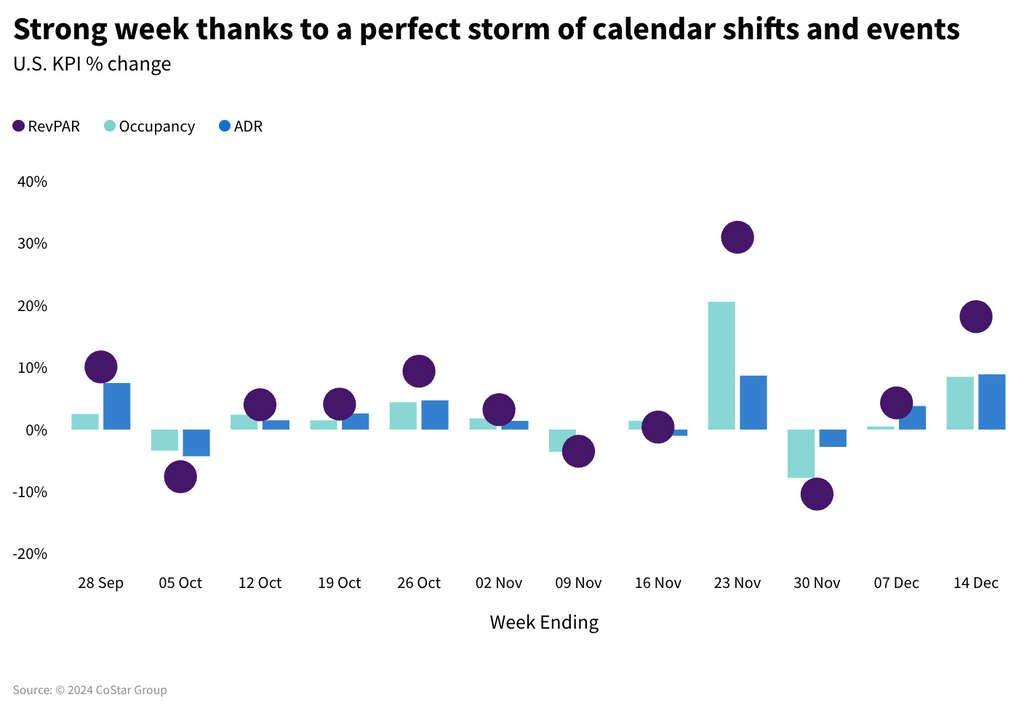

A perfect storm of factors

U.S. hotel industry revenue per available room (RevPAR) rose a whopping 18.2% during the week ending 14 December 2024. This was the highest weekly RevPAR gain since February 2023 (excluding a recent week that was skewed by the Thanksgiving calendar shift). The strong performance was seen across the industry, driven largely by an 8.9% gain in average daily rate (ADR), which was the highest for the industry since February 2023. Occupancy also showed robust growth, up 4.7 percentage points (ppts).Each day of the week produced strong RevPAR growth, ranging from +12.8% on Saturday to +22.6% on Tuesday, and nearly all U.S. markets (88%,149 out of 171) reported RevPAR growth, including 24 of the Top 25 Markets.

Several factors contributed to this noteworthy performance:

The shortened period between Thanksgiving and Christmas, as well as the year-over-year shift in the Hanukkah calendar, made for a clean week for business travelers and meeting planners to conduct business and hold events. As noted before, since March, the 2024 calendar matches perfectly with 2019. If you look back at that year, the corresponding week also increased significantly (RevPAR: +11.9%) with 78% of all markets seeing growth.

Group demand increased 47.5% compared to the same week last year. In 2019, group demand growth was also noteworthy, increasing 34.5% YoY.

Holiday parties have become a more significant travel event with remote workers gathering for company celebrations. The clean week provided a window of time to gather before employees started their vacations.

The U.S. election paused travel for a week in early November, which was most likely recovered in subsequent weeks, including this one.

Hurricane-affected markets continue to see RevPAR gains with seven markets throughout the Carolinas, Georgia and Florida posting a 50.3% increase in RevPAR.

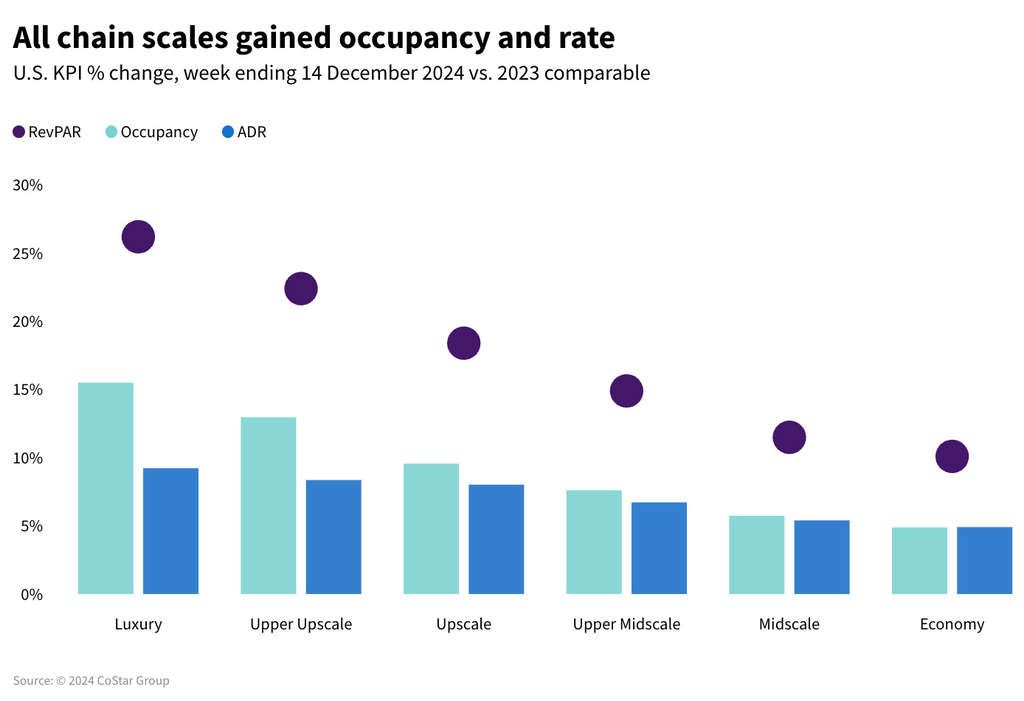

All chain scales increased RevPAR for the second consecutive week, boosted by both occupancy and ADR. Luxury hotels (+26.2%) led with the largest gain, while Economy (+10.1%) reported the smallest increase. Occupancy gains in the chain scales ranged from +9.4ppts in Luxury to +2.3ppts for Economy. ADR increases also had a similar distribution, rising 9.2% in Luxury hotels to 4.9% for Economy hotels.

Weekday (Monday – Wednesday) RevPAR advanced the most (+21.3%), followed by shoulder days (Sunday and Thursday) at +17.6%, and weekends (Friday/Saturday) at +14.3%. This pattern held true across the top four chain scales (Luxury – Upper Midscale) along with Independents, with the largest variation in Luxury chains (+33.1% weekdays vs. +17.2% weekends). Midscale and Economy were a bit different as the weekend showed the largest RevPAR growth.The number of markets reporting weekly RevPAR growth (149) was the most since the week ending 4 February 2023. Market highlights included:

Washington D.C. topped the Top 25 Market list with RevPAR increasing 67.6%. The annual American Geophysical Union (AGU), which rotates cities, lifted performance through both ADR (+26.8%) and occupancy (+18.7ppts).

San Francisco hosted the AGU event last year, and its absence led to a RevPAR decline. San Francisco was the only Top 25 Market with a decrease for the week.

Tampa continued to see strong performance with RevPAR up 60% YoY. Hurricane recovery in addition to group travel (+5.8 ppts YoY) and other activity in the contributed to this performance.

New York City posted the second highest actual RevPAR of the year ($476), up 35% from a year ago. Weekdays showed the strongest performance with Tuesday RevPAR increasing 52.5% on a 44.9% ADR increase. Occupancy in NYC was 93.3%, its second highest weekly level of the year. Tuesday and Wednesday occupancy each topped 96% with Tuesday reaching 97.4%, close to the 2024 high seen on 16 October 2024 (98%). The highest occupancy ever recorded for New York City was 98.8% in October 2000. Finally, New York has had the nation’s highest occupancy in 24 of the past 50 weeks and in the past five consecutive weeks.

Orlando experienced 26.7% RevPAR growth via Group occupancy increasing 10.5 ppts YoY.

Augusta led the entire nation in RevPAR growth (+71.6%). This market continued to see strong demand due to Hurricane Helene recovery efforts while also conducting normal business as evidenced by its hosting of the 78th annual Southeastern Association of Fish and Wildlife Agencies (SAFWA) conference.

Compressed holiday period lifted group demand

The strong group demand seen in Augusta represents one of many markets across the country hosting conferences and events during a time of year that is typically slow due to the holidays. U.S. group demand in Luxury and Upper Upscale hotels increased 47.5% compared to the same week last year. In 2019, with the same calendar composition, group demand increased 34.5%, indicating that this gain was not unexpected, However, the magnitude of the growth was a surprise and believed to be impacted by the above-mentioned factors. For context, the highest group demand week of the year was 2.4 million group rooms in October compared to 1.7 million group rooms this week.

Second highest Global RevPAR gain of the year

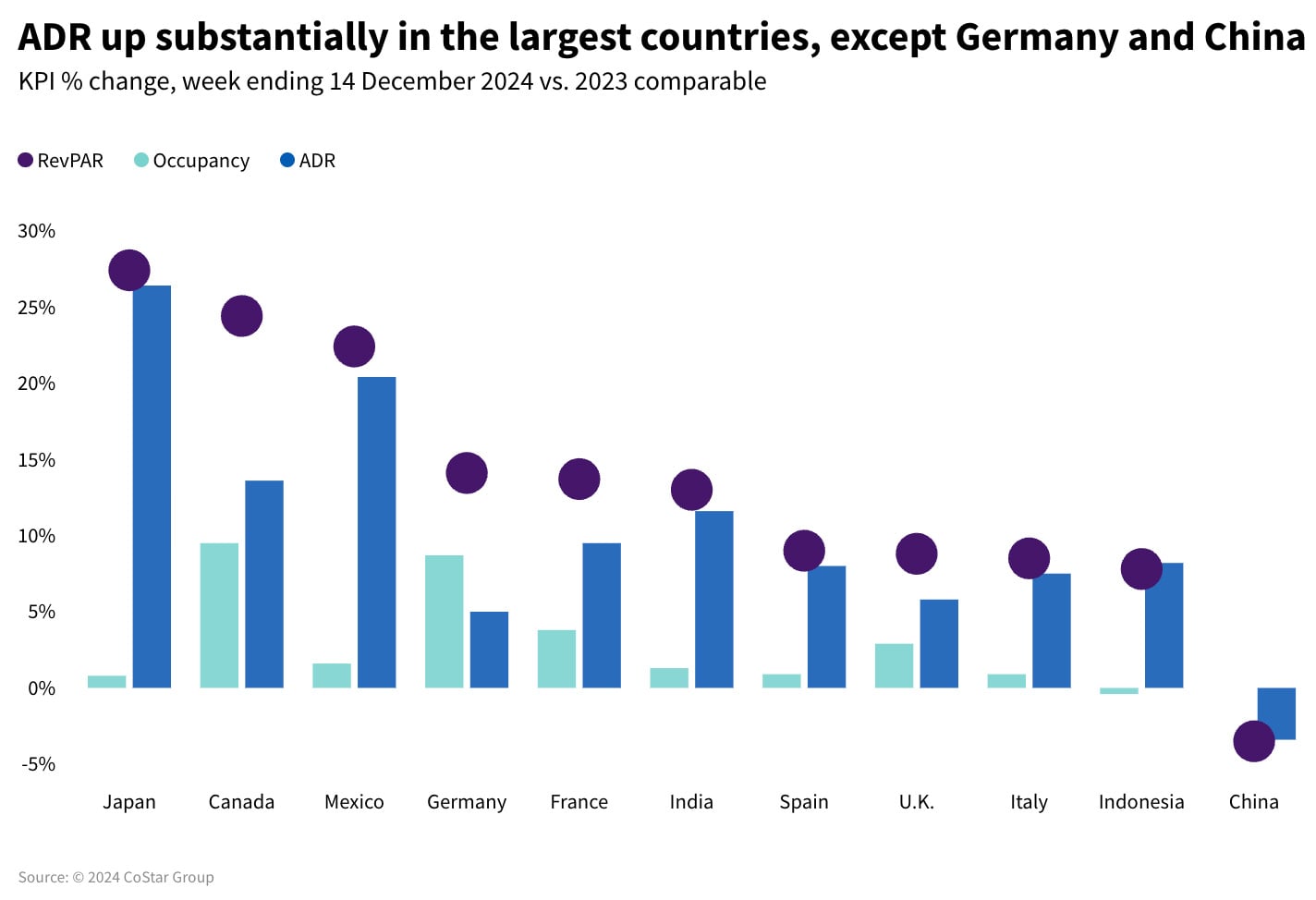

Global RevPAR, excluding the U.S., showed its largest increase (+12%) since February 2024 and has been holding close to this level for the past 19 weeks, which is above the YTD RevPAR growth level (+6.8%). ADR continued to be the primary driver, advancing 8.4% while occupancy came in with its largest gain (2.1 ppts) since early November. Across the largest countries in terms of room supply:

Japan continued to post robust RevPAR, increasing 27.4% entirely on ADR (+26.4%). All but two of the 11 Japanese markets recorded double-digit RevPAR growth with Kyoto and Tokyo posted the greatest gains.

RevPAR in Canada rose 24%, lifted in part by the final concert of Taylor Swift’s Eras Tour in Vancouver. RevPAR in Vancouver increased 133.9% with ADR rising 69.7% to $256. ADR over the three concert days averaged $632 with average occupancy of 85.7%. Taylor Swift wasn’t the only thing happening in Vancouver. Occupancy remained strong for the rest of the week, ranging from 85% on Monday to 93% on Saturday.

Mexico continued to see strong RevPAR growth, up 22.6% for the week. Robust performance has been seen for the past three weeks with RevPAR gains averaging 28.3%. Nearly all markets saw solid RevPAR gains with Baja California, Mexico City and Yucatan seeing the largest.

Germany experienced a strong week with RevPAR increasing 12.5%, the result of ADR increasing 4.5% and occupancy up 5.1ppts. The strong occupancy growth is atypical of the trends seen throughout the largest countries where ADR has been the driver and not occupancy.

China posted a RevPAR decline of 3.5% due entirely to ADR and, while in decline, the past two months have seen less negative RevPAR compared to Q3 (-9.2%) and Q2 (-5.7%).

Final Thoughts

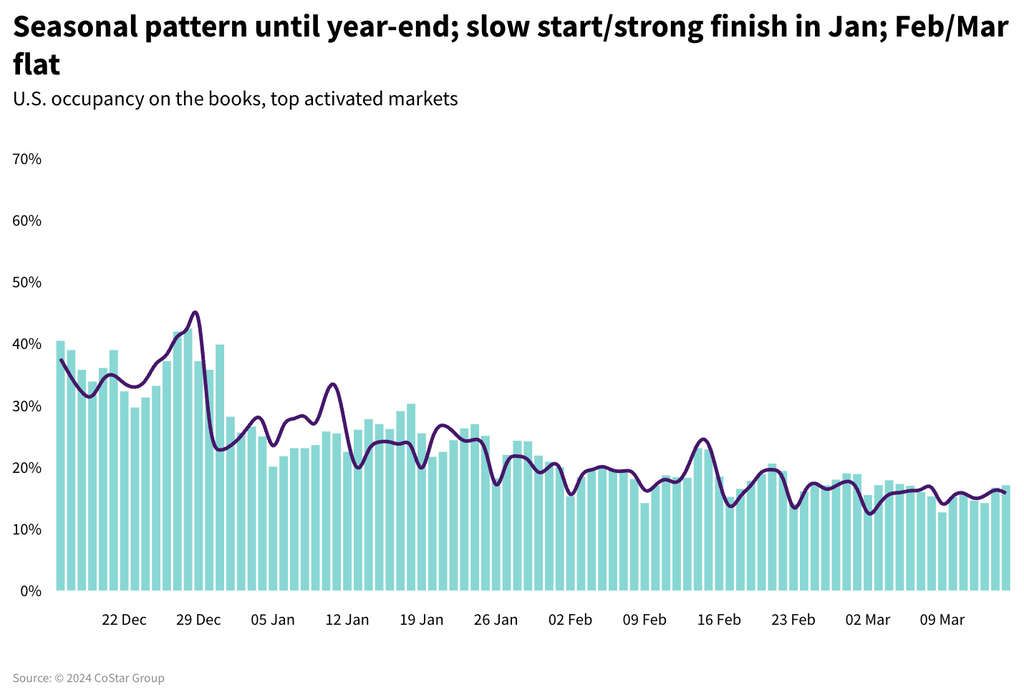

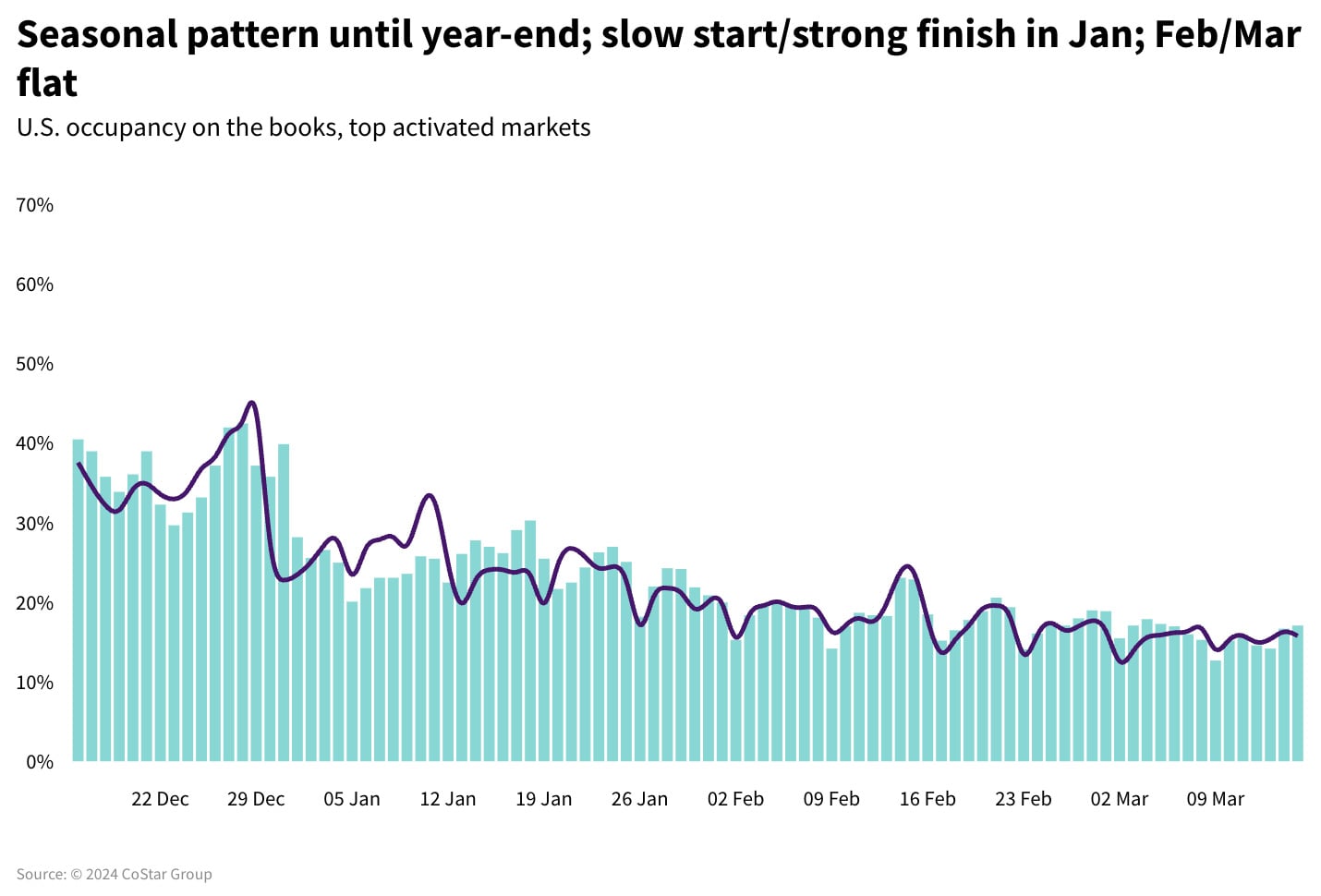

This week’s strong performance was a bit of a surprise. We knew it would be good due to the compressed period between Thanksgiving and Christmas, but we didn’t expect it to be that good. The last two weeks of the year are predicted to show modest growth due to the movement of Christmas and New Year’s to Wednesday from Monday a year ago. That said, this week was a surprise, so there could be more overperformance on the way.Looking further ahead, occupancy on the books in January is a net positive with a slow start and a strong finish. February and March are looking flat. We expect higher growth levels in March because the Easter and Passover observances occur in April next year. Global performance seems unstoppable and is expected to continue growing RevPAR through ADR for the foreseeable future.

Analysis by Isaac Collazo, Chris Klauda Note: Due to the holidays, the next edition of Weekly Insights will run on 10 January 2025. All financial figures represent US dollar.

About CoStar Group, Inc.

CoStar Group (NASDAQ: CSGP) is a leading provider of online real estate marketplaces, information, and analytics in the property markets. Founded in 1987, CoStar Group conducts expansive, ongoing research to produce and maintain the largest and most comprehensive database of real estate information. CoStar is the global leader in commercial real estate information, analytics, and news, enabling clients to analyze, interpret and gain unmatched insight on property values, market conditions and availabilities. Apartments.com is the leading online marketplace for renters seeking great apartment homes, providing property managers and owners a proven platform for marketing their properties. LoopNet is the most heavily trafficked online commercial real estate marketplace with thirteen million average monthly global unique visitors. STR provides premium data benchmarking, analytics, and marketplace insights for the global hospitality industry. Ten-X offers a leading platform for conducting commercial real estate online auctions and negotiated bids. Homes.com is the fastest growing online residential marketplace that connects agents, buyers, and sellers. OnTheMarket is a leading residential property portal in the United Kingdom. BureauxLocaux is one of the largest specialized property portals for buying and leasing commercial real estate in France. Business Immo is France’s leading commercial real estate news service. Thomas Daily is Germany’s largest online data pool in the real estate industry. Belbex is the premier source of commercial space available to let and for sale in Spain. CoStar Group’s websites attracted over 163 million average monthly unique visitors in the third quarter of 2024. Headquartered in Washington, DC, CoStar Group maintains offices throughout the U.S., Europe, Canada, and Asia. From time to time, we plan to utilize our corporate website, CoStarGroup.com, as a channel of distribution for material company information. For more information, visit CoStarGroup.com.

This news release includes “forward-looking statements” including, without limitation, statements regarding CoStar’s expectations or beliefs regarding the future. These statements are based upon current beliefs and are subject to many risks and uncertainties that could cause actual results to differ materially from these statements. The following factors, among others, could cause or contribute to such differences: the risk that future media events will not sustain an increase in future occupancy rates. More information about potential factors that could cause results to differ materially from those anticipated in the forward-looking statements include, but are not limited to, those stated in CoStar’s filings from time to time with the Securities and Exchange Commission, including in CoStar’s Annual Report on Form 10-K for the year ended December 31, 2023 and Forms 10-Q for the quarterly periods ended March 31, 2024, June 30, 2024, and September 30, 2023, each of which is filed with the SEC, including in the “Risk Factors” section of those filings, as well as CoStar’s other filings with the SEC available at the SEC’s website (www.sec.gov). All forward-looking statements are based on information available to CoStar on the date hereof, and CoStar assumes no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise.

View source